Buying property still feels like paperwork from another century—weeks of back-and-forth emails, wet signatures, couriered documents, and too many parties to count. Blockchain and smart contracts flip that script by turning agreements into code and records into tamper-evident ledgers. In the next decade, title updates, escrow, payments, and even ongoing property management can become programmable, auditable, and faster—often minutes instead of months—without sacrificing legal enforceability.

This guide explains how the technology works in plain language and what it means for developers, brokers, investors, lenders, and regulators. You’ll learn the key use cases that are already moving from pilots to production, what it takes to get started, and how to measure success while staying compliant in multiple jurisdictions.

Disclaimer: The following is educational information, not legal, tax, or financial advice. Real estate and securities laws vary widely. Consult qualified counsel and licensed professionals before implementing any approach described here.

Key takeaways

- Smart contracts automate the most error-prone steps in conveyancing (escrow, signatures, disbursements, title updates) and can reduce closing times and costs.

- On-chain registries and tokenization enable more transparent ownership records and new capital formation models (fractional equity, programmable income).

- Legal rails exist today for e-signatures and remote notarization in many markets, enabling digital-first closings that integrate with blockchain-based workflows.

- Compliance-by-design—identity, KYC/AML, and audit trails baked into contracts—will separate viable deployments from experiments.

- Start small, measure ruthlessly (time-to-close, error rates, rework, disputes) and expand in phases once metrics beat your baseline.

Why blockchain matters in property deals (and what it is)

What it is & core benefits

Blockchain is a shared, append-only database. Once data is recorded, it’s extremely difficult to alter without consensus. Smart contracts are code that runs on top of a blockchain and enforces terms automatically (for example, releasing escrow when a deed is recorded). For real estate, the big wins are:

- Integrity: An auditable trail of offers, approvals, funds, and filings.

- Speed: Programmed steps reduce waiting on manual handoffs.

- Interoperability: APIs unify brokers, lenders, title offices, and registries.

- Programmability: Leases, mortgages, liens, and rights become machine-executable logic.

Requirements/prerequisites

- A blockchain network (public or permissioned) and smart contract platform.

- Wallet infrastructure for authorized parties; secure key management.

- Integrations with identity providers, e-signature/notary services, payment rails, and (ideally) land registries.

- Legal review aligned to local statutes for signatures, notarization, and securities.

Beginner steps

- Map your current closing workflow step-by-step (who does what, when, with what system).

- Choose one narrow process to automate (for example, earnest money escrow).

- Implement a basic smart contract that holds funds and releases upon documented conditions.

- Plug in e-signature and remote notarization where permitted.

- Pilot with a single property and willing counterparties; monitor KPIs.

Beginner modifications & progressions

- Simplify: Start read-only—hash documents to the chain for integrity proofs before automating funds.

- Scale: Move from escrow to full “offer-to-deed” with title updates and automated payments.

Recommended metrics

- Days to close; number of email/call touches per file; error/rework rate; disputes; cost per transaction.

Safety & common mistakes

- Over-automating before aligning with registry law.

- Poor key custody practices.

- Ignoring consumer consent and notice requirements in digital signature flows.

Mini-plan example (2–3 steps)

- Step 1: Hash purchase agreements on-chain for tamper evidence.

- Step 2: Add a simple escrow smart contract with clear release conditions.

On-chain title & land registries

What it is & core benefits

Digitally anchoring deeds, transfers, and encumbrances to a blockchain creates a tamper-evident record of title. Some governments and registries have run proofs-of-concept and pilots showing faster conveyancing and improved integrity.

Benefits: resilient audit trails, simplified due diligence, reduced fraud risk, and faster registry updates.

Requirements/prerequisites

- Legal mandate or partnership with the land registry.

- Standard data model for parcels, owners, liens, and timestamps.

- Governance (who can write/update), privacy controls, and disaster recovery.

- Integration with existing registry databases and public portals.

Implementation steps (beginner)

- Mirror, don’t move: Start by hashing registry entries to the chain (integrity proofs) without replacing the official database.

- Build a write API that submits registry updates as both database entries and blockchain events.

- Publish a public viewer that can verify the hash of a deed or title certificate.

- Expand to include transfer events and lien releases.

Modifications & progressions

- Private → Public anchoring: Use a permissioned ledger for performance and anchor periodic snapshots to a public chain for additional integrity.

- Automation: Trigger smart contracts when registry confirms receipt (e.g., escrow release).

Frequency/metrics

- % of deeds hashed on-chain, registry update latency, verification requests per month, detected discrepancies.

Safety & common mistakes

- Treating an on-chain record as legally dispositive before statute says so.

- Publishing personal data without privacy-by-design (store hashes, not raw documents).

Mini-plan

- Step 1: Hash all new registry entries and publish a verification tool.

- Step 2: Pilot automated escrow release upon confirmed registry update.

Smart-contract escrow & automated closings

What it is & core benefits

Escrow is a rules-and-money problem—perfect for automation. Smart contracts can hold buyer funds in a wallet, release them when title conditions are met, pay out participants, and log everything immutably.

Benefits: fewer errors, instant disbursements, lower operational costs, clearer audit trails, reduced fraud.

Requirements/prerequisites

- Banking or stablecoin rails, depending on jurisdiction.

- Licensed escrow agent or supervised financial partner.

- Identity/KYC and sanctions screening.

- Connection to title verification and e-recording where available.

Implementation steps

- Create a smart contract template for earnest money with whitelisted participants.

- Implement condition checks: signatures collected, title cleared, registry receipt confirmed.

- Connect to payment rails: fiat via bank API or regulated stablecoin.

- Automate payouts to seller, taxes, commissions.

Modifications & progressions

- Beginner: Only automate escrow deposits and refunds.

- Advanced: End-to-end “click-to-close” where signatures, escrow, registry updates, and disbursements fire in one flow.

Metrics

- Average time from offer acceptance to disbursement; number of funding errors; fee savings per file.

Safety & mistakes

- Unclear refund logic; failure to handle contingencies; missing consumer disclosures.

- Deploying unaudited smart contracts.

Mini-plan

- Step 1: Launch a limited escrow pilot using a regulated stablecoin with KYC’d buyers.

- Step 2: Add auto-disbursement when a registry webhook confirms title is updated.

Tokenization & fractional ownership

What it is & core benefits

Tokenization represents ownership interests as digital tokens. These can reflect equity in a property SPV, revenue-sharing claims on rent, or debt interests. Fractionalization lowers investment minimums, broadens access, and enables programmable compliance and distributions.

Requirements/prerequisites

- Corporate structure (SPV) that holds the property.

- Securities compliance (offering exemptions or prospectus/registration, transfer restrictions).

- Transfer agent or cap table logic in smart contracts.

- Custody of investor tokens and secondary trading rules (where permitted).

Implementation steps

- Define the instrument (equity, debt, income share) and its rights.

- Encode transfer restrictions (whitelists, lockups) in the token contract.

- Build distribution logic for rent/dividend payouts and investor dashboards.

- Onboard investors via KYC/AML checks; issue tokens upon subscription.

- If allowed, list on a regulated venue for secondary liquidity.

Modifications & progressions

- Starter: Private, closed investor group—no secondary trading.

- Next: Permissioned secondary trading via a licensed ATS or MTF.

Metrics

- Capital raised vs. traditional route, investor acquisition cost, secondary volume, payout accuracy.

Safety & mistakes

- Marketing as “utility” to avoid securities rules.

- Failing to reconcile on-chain cap tables with legal records.

- Ignoring tax treatment of tokenized distributions.

Mini-plan

- Step 1: Tokenize a single-asset SPV with built-in quarterly rent distributions.

- Step 2: Add compliance checks for secondary transfers after a lockup period.

Digital identity, e-signatures & remote notarization

What it is & core benefits

Signatures and notarization are essential legal steps. Today, widely accepted e-signature laws and, in many jurisdictions, remote online notarization (RON) enable fully digital closings that integrate with smart contracts.

Benefits: fewer in-person appointments, faster execution, clear consent and audit logs, and better accessibility for cross-border parties.

Requirements/prerequisites

- e-signature platform supporting advanced/qualified signatures where required.

- Video notarization and identity proofing that meets local laws.

- Consent workflow, document retention, and long-term validation (LTV) of signatures.

Implementation steps

- Configure signature policies aligned to your jurisdiction (standard, advanced, or qualified).

- Build RON into the closing flow where permitted.

- Hash signed documents to the blockchain for integrity evidence.

- Store originals in a compliant repository with time-stamps.

Modifications & progressions

- Basic: Electronic signatures only.

- Full: e-sign + RON + on-chain hashing + automated smart-contract steps.

Metrics

- % of documents fully digital, signer completion times, notarization scheduling latency, error rate (missing initials, mis-signed pages).

Safety & mistakes

- Assuming e-signatures are identical across jurisdictions.

- Storing personally identifiable information on-chain instead of hashing.

Mini-plan

- Step 1: Move all offers, addenda, and disclosures to e-sign with tamper-evident logs.

- Step 2: Add RON for closing packages in jurisdictions that allow it, and anchor hashes on-chain.

Smart leases & property management

What it is & core benefits

Leases can be encoded as smart contracts that calculate and collect rent, apply late fees, escalate rates, and route funds to landlords, managers, and lenders. Maintenance requests, deposits, and access rights can be tracked on-chain.

Benefits: fewer back-office hours, faster collections, improved transparency for tenants, and real-time financial data for owners and lenders.

Requirements/prerequisites

- Payment rails with low-cost recurring transfers.

- Tenant identity verification and screening integrations.

- Oracles for CPI or index-linked escalations.

Implementation steps

- Create a smart lease template with base rent, deposits, escalation schedule, and penalties.

- Connect to ACH or compliant stablecoin rails.

- Build a tenant portal to view balances and initiate maintenance requests.

- Add automated notices and receipts.

Modifications & progressions

- Starter: Record payments and deposits on-chain, keep lease PDF off-chain.

- Advanced: Full lease logic on-chain with role-based access and IoT-linked conditions (e.g., key delivery on payment).

Metrics

- Days sales outstanding (DSO), delinquency rate, maintenance ticket SLA, tenant satisfaction.

Safety & mistakes

- Hardcoding terms that need discretion or legal notice.

- Failing to handle partial payments or payment plan accommodations.

Mini-plan

- Step 1: Automate deposit handling and refund rules as a smart contract.

- Step 2: Add recurring rent debits with transparent on-chain receipts.

Mortgages, liens & programmable finance

What it is & core benefits

Mortgages and liens can be represented as digital instruments with programmable covenants: interest accrual, payment waterfalls, and lien releases synchronize with registry updates. This improves collateral tracking and reduces servicing errors.

Requirements/prerequisites

- Legal templates for digital promissory notes and lien filings.

- Servicing platform integration (escrow, taxes, insurance).

- Oracles for rates, indices, and credit events.

Implementation steps

- Issue a digital note with embedded logic for interest, amortization, and prepayment.

- Link lien status to the land registry; release upon final payment automatically.

- Integrate payment rails and investor reporting for securitized pools.

- Pilot with a small number of loans and clear forbearance playbooks.

Modifications & progressions

- Basic: On-chain lien releases only.

- Advanced: Full mortgage lifecycle with investor pass-throughs and real-time reporting.

Metrics

- Time from payoff to lien release, servicing error rate, investor reporting latency, cost per loan.

Safety & mistakes

- Failing to model loss mitigation and regulatory change.

- Misaligning on-chain status with official filing systems.

Mini-plan

- Step 1: Automate lien release filings tied to final payment confirmation.

- Step 2: Expand to programmable payment waterfalls for small private notes.

Data, due diligence & oracles

What it is & core benefits

Oracles feed smart contracts with trusted external data—inspections, valuations, flood maps, tax liens, and compliance results. Digitizing due diligence packages and anchoring their hashes on-chain ensure what everyone sees is what was agreed at closing.

Benefits: less rework, fewer version conflicts, better risk controls.

Requirements/prerequisites

- Credentialed data providers and API agreements.

- Document hashing standards, content-addressed storage (e.g., IPFS gateways or cloud with content checks).

Implementation steps

- Define required due diligence artifacts and data feeds.

- Hash each artifact at upload; store hash and metadata on-chain.

- Build rule checks (e.g., property taxes current before disbursement).

- Maintain an audit trail of who accessed what and when.

Modifications & progressions

- Basic: Hash-only evidence with off-chain storage.

- Advanced: Zero-knowledge proofs to validate facts (e.g., “taxes paid”) without disclosing the documents.

Metrics

- Document mismatch rate, missing-doc rework, time from “DD complete” to close.

Safety & mistakes

- Assuming oracle data is infallible; always include dispute and override processes.

- Storing sensitive PDFs on-chain.

Mini-plan

- Step 1: Hash all due diligence documents on-chain.

- Step 2: Add rule-based checks that block disbursement if required data is stale or missing.

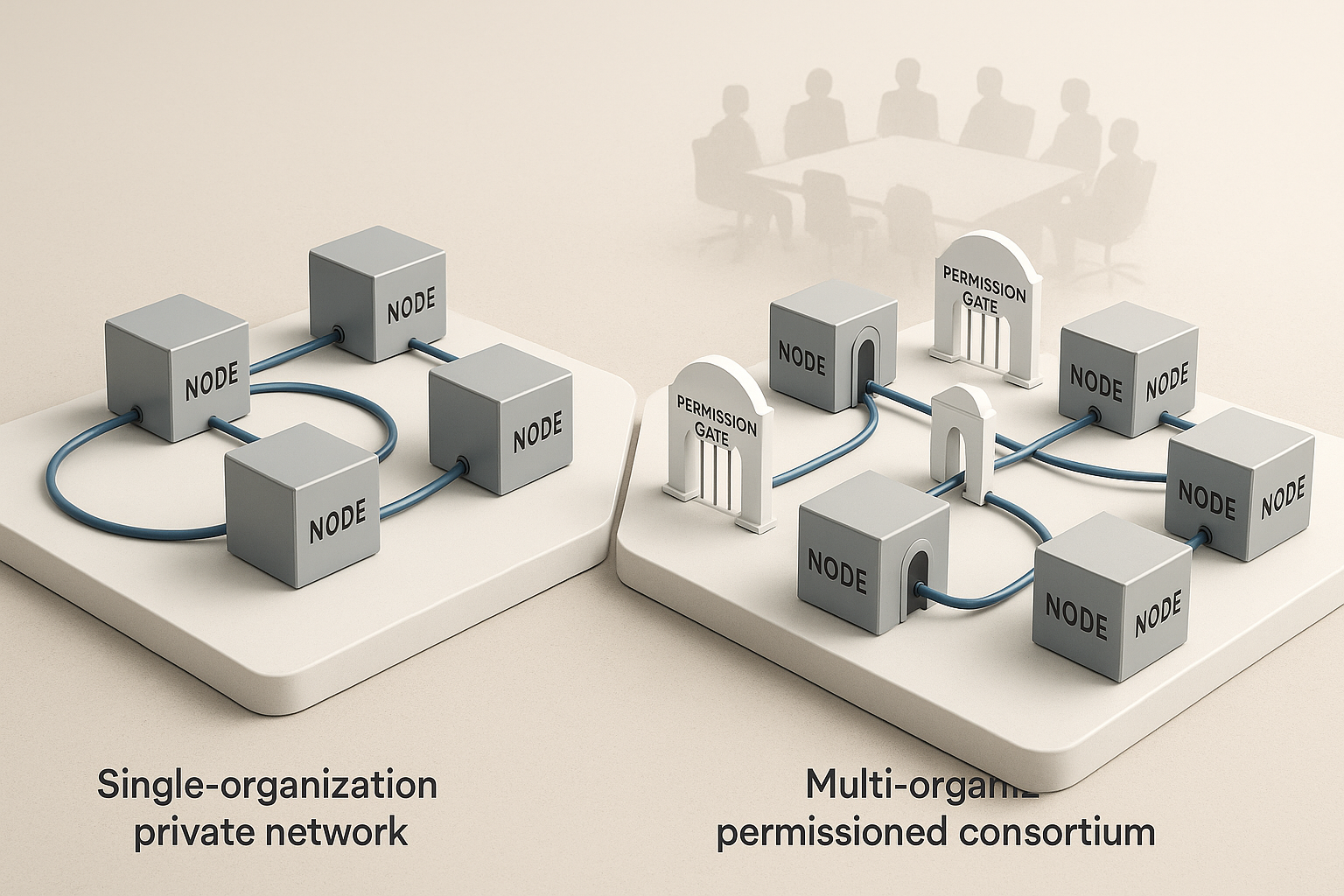

Public vs. permissioned chains & interoperability

What it is & core benefits

Public chains maximize transparency and censorship resistance. Permissioned chains offer controlled participation, privacy, and throughput. Many real estate deployments blend both: transact privately, anchor proofs publicly.

Benefits: compliance and performance without giving up global verifiability.

Requirements/prerequisites

- Clear data classification and privacy policy.

- Bridging or anchoring strategy between networks.

- Vendor-neutral standards for data schemas and event logs.

Implementation steps

- Categorize data: public, restricted, confidential.

- Choose a permissioned ledger for sensitive events; anchor hashes to a public chain periodically.

- Use standard interfaces for portability.

- Document exit and recovery procedures if a network sunsets.

Modifications & progressions

- Start: Single chain with public anchoring.

- Scale: Multi-chain or L2 strategy with interoperability libraries.

Metrics

- Anchoring frequency, audit pass rates, privacy incidents, chain uptime.

Safety & mistakes

- Vendor lock-in with proprietary schemas.

- Over-sharing personal data on public networks.

Mini-plan

- Step 1: Anchor weekly state hashes from your permissioned ledger to a public chain.

- Step 2: Implement a portable export of all events for disaster recovery.

Quick-start checklist

- Define one micro-use case (escrow, lien release, or document hashing).

- Confirm legal basis for e-signatures and notarization in your jurisdiction.

- Choose network approach (permissioned + public anchoring is a practical default).

- Stand up identity/KYC and payment integrations first.

- Commission a smart contract audit and incident response plan.

- Draft consumer disclosures and consent flows.

- Establish KPIs: time-to-close, touches, errors, disputes, cost per file.

- Run a single-asset pilot, then a postmortem, then scale.

Troubleshooting & common pitfalls

- “Our registry won’t accept on-chain records.” Start with hash anchoring and dual-write to existing systems. Seek sandbox MOUs before production.

- “Legal said no.” Narrow scope to integrity proofs and digital signatures already accepted by statute; expand once comfortable.

- “The stablecoin isn’t allowed.” Use bank rails first; design contracts that are payment-rail agnostic.

- “Data privacy fears.” Put only hashes and event IDs on-chain; keep documents off-chain with strict access control.

- “Smart contract bugs.” Use templates, audits, and staged rollouts with kill switches and manual overrides.

- “User friction with wallets.” Custodial wallets for supervised processes and role-based access can reduce complexity.

How to measure progress (and prove ROI)

Track before-and-after comparisons on:

- Cycle time: offer → close; payoff → lien release.

- Quality: % of files closed with zero rework; dispute rate per 100 closings.

- Cost: escrow/closing fees per file; staff hours per closing.

- Risk: fraud incidents; data mismatch rates; audit findings.

- Adoption: % of documents digitally signed; % of closings with RON; % of deals with on-chain hashes.

Set quarterly targets (for example, reduce rework 30%, cut closing time by 25%, increase digital-signature adoption to 90%).

A simple 4-week starter plan

Week 1 – Map & select

- Map the current closing workflow and pick one step (e.g., earnest-money escrow) to automate.

- Choose your tech stack (signature, notary, blockchain, custody).

- Draft risk assessment and success metrics.

Week 2 – Build & integrate

- Deploy a basic smart contract for escrow or document hashing.

- Integrate identity, KYC, and e-signature.

- Prepare consumer disclosures and internal SOPs.

Week 3 – Pilot

- Run one test transaction with internal stakeholders or a friendly client.

- Capture cycle time, errors, and user feedback.

Week 4 – Review & expand

- Compare KPIs to baseline; fix gaps.

- Decide whether to add registry anchoring, auto-disbursement, or RON.

- Plan the next 90-day rollout.

Frequently asked questions

1) Is a blockchain deed legally valid?

It depends on jurisdiction. Many places accept e-signatures and electronic records; some registries are piloting blockchain-based processes. In most markets today, the official record remains the government’s registry, but blockchain can provide integrity proofs and automation alongside it. See the references for examples and current frameworks.

2) Do we need cryptocurrency to use smart contracts?

No. You can use bank rails for payments and still run smart contracts for logic and audit trails. Stablecoins or tokenized deposits can be used where permitted, but they are optional.

3) Which chain should we use?

Pick based on governance and data needs. If privacy and controlled access are critical, start permissioned and anchor hashes to a public chain for verifiability. Ensure exportability to avoid lock-in.

4) How do we handle privacy laws when storing data on-chain?

Do not store personal data or full documents on-chain. Store hashes and minimal metadata, keep documents off-chain in compliant storage, and use strict access controls.

5) Are e-signatures enough, or do we need special “blockchain signatures”?

Standard e-signatures that meet local laws are usually sufficient. You can hash the signed document on-chain to prove integrity, but the legal validity stems from signature law, not the blockchain itself.

6) What about remote online notarization?

Many U.S. states and some other jurisdictions allow RON. Check local rules; build video ID proofing and retention policies that meet legal standards.

7) Can we really shorten closings from weeks to minutes?

Proofs-of-concept have shown dramatic reductions when registries, lenders, and brokers collaborate on a unified digital flow. Real-world timelines depend on your integrations and legal constraints.

8) How do tokenized real estate investments fit into securities law?

Tokenized interests are usually treated as securities and must follow offering, disclosure, and transfer rules. Build compliance controls (whitelists, lockups) into the smart contract and work with licensed venues for any secondary trading.

9) Will regulators in my region accept blockchain records?

Regulatory posture varies. Some authorities are running pilots and issuing guidance, and comprehensive crypto-asset frameworks now apply across parts of the world. Start with narrowly scoped, compliant uses and expand as rules mature.

10) What happens if a smart contract has a bug?

Use audited code, pre-deployment testing, limited pilots, and emergency controls. Always maintain an off-chain dispute mechanism and a human-in-the-loop for edge cases.

11) How do we migrate legacy deals to a new system?

Don’t. Start with new transactions. For legacy archives, hash existing PDFs on-chain to provide tamper evidence without altering official records.

12) What KPIs convince executives to scale?

Consistent reductions in time-to-close and rework, fewer disputes, cleaner audits, and fee savings per file. Tie these to a business case for expanding automation.

Conclusion

Real estate is full of steps that are perfectly suited to code: hold money, check conditions, sign here, record there, then pay everyone—cleanly and transparently. Blockchain and smart contracts don’t replace the law or the registry; they reinforce them with automation and verifiability. Start small, integrate with existing rails, measure everything, and expand when the numbers make it inevitable.

Call to action: Pilot one blockchain-enabled step in your next closing—hash the documents or automate escrow—and use the results to design your full digital roadmap.

References

- The Land Registry in the Blockchain (project report), ICA / Lantmäteriet partners, July 2016. https://ica-it.org/pdf/Blockchain_Landregistry_Report.pdf

- Blockchain-Based Land Titling Project in the Republic of Georgia, Innovations: Technology, Governance, Globalization (MIT Press), 2019. https://direct.mit.edu/itgg/article-pdf/12/3-4/72/705280/inov_a_00276.pdf

- HM Land Registry to explore the benefits of blockchain, UK Government, October 1, 2018. https://www.gov.uk/government/news/hm-land-registry-to-explore-the-benefits-of-blockchain

- Could blockchain be the future of the property market?, HM Land Registry Blog, May 24, 2019. https://hmlandregistry.blog.gov.uk/2019/05/24/could-blockchain-be-the-future-of-the-property-market/

- HM Land Registry – towards a distributed ledger of residential title deeds in the UK, Mishcon de Reya, July 2, 2020. https://www.mishcon.com/news/hm-land-registry-towards-a-distributed-ledger-of-residential-title-deeds-in-the-uk

- Real Estate Tokenisation Project (pilot announcement), Dubai Land Department, March 19, 2025. https://dubailand.gov.ae/en/news-media/dubai-land-department-launches-pilot-phase-of-the-real-estate-tokenisation-project/

- Real Estate Tokenization (overview page), Dubai Land Department, July 30, 2025. https://dubailand.gov.ae/en/eservices/real-estate-tokenization/

- Dubai Land Department achieves a technical milestone with the adoption of blockchain technology, Dubai Land Department, July 30, 2025. https://dubailand.gov.ae/en/news-media/dubai-land-department-achieves-a-technical-milestone-with-the-adoption-of-blockchain-technology-in-cooperation-with-smart-dubai-and-other-partners/

- Roofstock onChain Sells First Real Estate NFT Purchased with USDC through On-Chain Home Financing, GlobeNewswire, October 18, 2022. https://www.globenewswire.com/news-release/2022/10/18/2536481/0/en/Roofstock-onChain-Sells-First-Real-Estate-NFT-Purchased-with-USDC-through-On-Chain-Home-Financing.html

- Roofstock onChain (product site, transaction recap), accessed August 2025. https://onchain.roofstock.com/

- Markets in Crypto-Assets Regulation (MiCA) – ESMA overview, European Securities and Markets Authority, updated 2025. https://www.esma.europa.eu/esmas-activities/digital-finance-and-innovation/markets-crypto-assets-regulation-mica

17 Comments